The ultimate guide to the M&A process

TL;DR: What you need to know about the M&A process

- M&A success is decided early: clear deal thesis, tight screening, and proactive sourcing beat late-stage “fixes.”

- The M&A process runs through eight stages, from strategy and target research to LOI, diligence, and post-merger integration.

- Pre-qualification screening eliminates 50-80% of unsuitable targets early.

- Top acquirers build intent-driven target lists and start owner relationships months before companies formally go to market.

- Smart advisors qualify targets with strict financial, strategic, and cultural criteria, prioritizing exit-readiness signals over raw lead volume.

- Automation supports data gathering, filtering, and outreach cadences but can’t replace judgment or relationship-building.

- Consistent, personalized outbound plus disciplined pipeline stages and metrics creates predictable deal flow and higher close rates.

Most M&A guides focus entirely on legal documents and financial models while completely skipping the phase that matters most: finding the right targets before formal processes even begin.

M&A advisors and business owners often miss the systematic deal sourcing that separates successful acquirers from those stuck with overpriced, poor-fit targets (and we've all seen those deals).

So in this guide, we'll cover the complete M&A process from start to finish, including the eight core stages.

You'll learn what experienced advisors do differently when sourcing opportunities, how to build a systematic approach to finding quality deals, and why 50 to 90% of M&A transactions fail to deliver intended value.

And more importantly, you'll see how to avoid becoming another statistic in that failure rate. ✅

What is M&A and how does the process really work?

M&A, or mergers and acquisitions, is the umbrella term for transactions where companies combine (merger) or one company buys another (acquisition) as part of a growth or exit strategy.

People often use "merger" and "acquisition" interchangeably like they mean the same thing. They don't, and the difference matters when you're structuring a deal.

- A merger happens when two companies combine to create one brand-new legal entity. Both original companies stop existing. Shareholders from both sides get ownership in the new combined company, usually split proportionally based on what each side brought to the table. Both parties have to agree because you can't force someone into a merger.

- An acquisition is simpler: one company buys another. The buyer needs at least 51% of the target's stock to control decisions, though most deals involve buying 100%. Unlike mergers, acquisitions can be hostile. If management won't sell, a buyer can go straight to shareholders with an offer.

Why does this distinction matter for you?

Because the M&A deal cycle looks completely different depending on which side you're on. Buy-side advisors spend their time analyzing targets, building financial models, and trying not to overpay. Sell-side advisors control timing, manage competition between buyers, and push for the highest price.

In this guide, we’ll mostly cover the sell-side.

Why the M&A process starts before first contact

Most advisory firms wait for deals to show up. That's a mistake if you want access to quality targets at reasonable prices.

The firms closing great deals start their work months before formal processes begin. They're building market intelligence, developing relationships with business owners, and positioning themselves as trusted advisors before anyone mentions selling. 🎯

Research shows something interesting: you can eliminate 50 to 80% of potential targets early by using well-designed screening criteria. 🔍

That means you avoid wasting six months on a company that was never going to work because the financials don't support your thesis, the owner isn't actually ready to sell, or the cultural fit is terrible.

The quality of your M&A outcomes gets decided before anyone signs an NDA. When you've already invested time understanding a target, built relationships with key people, and developed real conviction around strategic fit, you enter negotiations with massive advantages. Those advantages matter way more than clever legal terms in the purchase agreement.

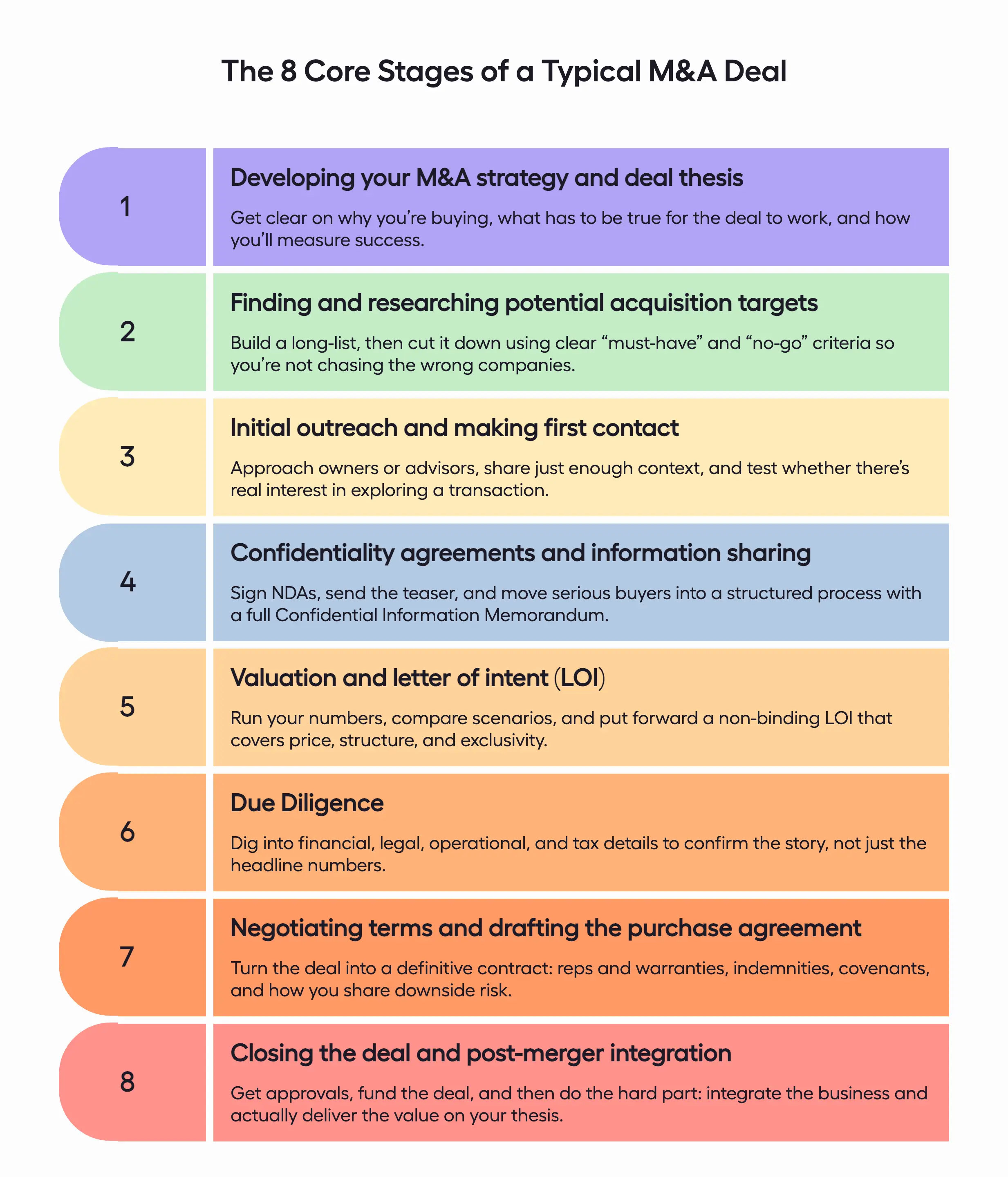

What are the key 8 stages of the M&A process?

The M&A process moves through eight distinct stages. Each one has specific activities, realistic timelines, and decision points where deals either move forward or die quietly (usually because someone found something ugly in due diligence).

Every transaction is different based on industry, company size, and regulatory complexity.

That said, this framework keeps deals moving systematically from your initial strategy through post-merger integration where you either create value or watch it evaporate.

Let's break down each stage so you know what to expect and how to prepare. 👇

Stage 1: Developing your M&A strategy and deal thesis

Every acquisition that creates value starts with a clear deal thesis. Not vague talk about synergies, but specific answers to hard questions.

- ⚠️ What business problem does this acquisition solve?

- ⚠️ What competitive advantage does the target bring that you can't build internally?

- ⚠️ What synergies can you realistically achieve?

- ⚠️ What risks could blow up the deal after closing?

You'll define what you're looking for, figure out how you'll finance deals, clarify your post-acquisition operating model, and identify who needs to be involved. This typically takes 2 to 6 months for companies running systematic acquisition programs.

Your deal thesis needs to get specific about value creation. Say you're planning to cross-sell your products to the target's customers. Specify which customer segments, which products, what conversion rates based on your historical data, and what customer churn to expect.

Stage 2: Finding and researching potential acquisition targets

This stage usually takes 1 to 3 months, depending on how much prep work you’ve already done.

You’ll start by building a list of companies that fit your acquisition strategy. Then you’ll narrow it down through screening and prioritization, focusing on strategic alignment and the potential to create value.

Once you’ve got a working shortlist, it’s time to reach out and gather data for early evaluation.

Nowadays M&A teams rely on intent-based targeting to surface signals that suggest a company might be ready for a conversation. When we help clients during this stage, we look at factors like founder tenure, company age, funding rounds, headcount shifts, and industry momentum.

This approach helps you spot opportunities before they go public, which gives you a head start and a stronger position.

Pro Tip: The best targets aren't on the market yet. Finding them before they enter formal sale processes means less competition and better pricing. 💡

Stage 3: Initial outreach and making first contact

Here’s what most M&A guides leave out: how do you actually start conversations with companies that aren’t for sale? 📧

Top advisors don’t sit back and wait. They’re proactive and methodical, using structured outreach that combines strategic thinking with disciplined follow-through. Deal flow doesn’t come from luck (even though plenty of people still act like it does).

Advisors who source quality opportunities use a mix of data and messaging that actually feels personal, applying cold email personalization tactics instead of generic copy-paste templates. They lead with surface-level insights, holding back on sensitive details until trust is established.

When we run lead gen for M&A clients, we focus on two things: deliverability and relevance. That means using real data ( like founder tenure, growth signals, funding activity) and building messages around it.

No mass-blast templates and no fluff. You show up as the advisor who clearly did their research (because you did), and that’s what gets the reply. ✉️

Wondering what to actually say in that first email to an owner you’ve never met? You’ll probably find our guide on how to write the best cold email very useful!

Stage 4: Confidentiality agreements and information sharing

Once there’s early interest, the first step is getting an NDA in place. This sets the ground rules before anything sensitive gets exchanged.

The non-disclosure agreement is a legally binding contract. It lays out what counts as confidential, how long the restrictions last (usually 3 to 5 years), who can access the data, and what happens if it’s mishandled.

Once the NDA is signed, the real information flow begins. 📄

The seller shares a confidential information memorandum (CIM). This is the main document buyers use to assess the deal and shape initial offers. It usually includes:

- Financials

- Market positioning

- Customer and supplier info

- Management structure

The CIM is the core pitch deck for a sell-side deal. Its clarity and depth shape how serious buyers get, and how high the offers go.

Stage 5: Valuation and letter of intent (LOI)

Valuation is always one of the most sensitive parts of the deal. It sets the price tag, so naturally, there’s plenty of debate.

Advisors typically rely on three core methods:

- Comparable company analysis (what similar firms have sold for)

- Discounted cash flow (future cash flows, adjusted to today’s value)

- Precedent transactions (pricing from recent, similar deals)

Once there’s alignment, the buyer submits a letter of intent.

This marks the shift from exploratory talks to serious negotiation. While most of it isn’t legally binding, certain terms do carry legal weight immediately, especially confidentiality and exclusivity.

A typical LOI includes:

- Proposed purchase price

- Payment structure

- Target close date

- Due diligence scope

- Exclusivity period (usually 30 to 90 days)

The exclusivity clause stops the seller from talking to other buyers for a set period. Most LOIs clearly state which provisions are binding and which aren't.

Stage 6: Due diligence in M&A deals

Due diligence is when buyers go deep. They review every material part of the target before moving forward.

This phase typically lasts 4 to 8 weeks, but it often runs longer, especially for larger or more complex businesses.

More diligence = more issues found = more negotiation. That often means the final price drops. 📊

There are four key categories:

Stage 7: Negotiating terms and drafting the purchase agreement

This is where the legal side takes center stage. The purchase agreement spells out every binding term of the deal.

It covers:

- Deal structure and closing mechanics

- Representations and warranties

- Indemnification terms

- Operational restrictions before close (aka covenants)

Most middle-market purchase agreements include 25 to 40 seller reps. These cover key areas like:

- Legal authority to sell

- Capitalization and ownership

- Financial statement accuracy

- Material contracts

- IP rights

- Litigation and compliance

- Insurance coverage

If these representations turn out to be false or if the seller didn't disclose something, that's a breach of contract. So the best practice is disclosing everything upfront in disclosure schedules rather than letting the buyer discover problems after closing.

Stage 8: Closing the deal and post-merger integration

Closing is when the acquisition becomes official. Purchase price gets paid, ownership transfers, regulatory approvals come through, and integration starts.

And post-merger integration determines whether acquisitions create value or destroy it.

The biggest barriers are rarely technical. Cultural and integration challenges are often the biggest obstacles because you're merging different organizational cultures, processes, and systems.

For successful integration consider:

- Starting early with “clean teams” handling sensitive work

- Turning synergy goals into detailed, sequenced plans

- Using clear roadmaps, timelines, and metrics

The first 100 days post-close are critical for setting momentum and proving the deal thesis.

What's the most effective way to find companies for acquisition?

Smart sourcing combines multiple channels, because what works for one industry or deal type might fall flat in another.

Database platforms like ZoomInfo, PitchBook, Capital IQ, and SourceScrub provide broad market coverage for initial screening. These work well for identifying companies matching specific revenue ranges, growth rates, or technology stacks.

The limitation?

Everyone uses them, so you're competing with dozens of other buyers for the same targets. There's also a good percentage of data that's outdated or inactive contacts. Plus, the same database is sold to other PE firms and investment banks.

Industry relationships offer a different kind of edge.

Conferences, owner networks, attorneys, and accountants all help surface opportunities before they hit the market.

This route delivers warmer leads, but takes years to develop.

Direct outreach on the other hand, is still very underrated, and extremely effective.

We've helped M&A advisors build campaigns reaching hundreds of pre-qualified companies monthly, generating conversations with owners who weren't actively seeking buyers. But the key is personalization at scale (mentioning specific company events, headcount growth, or funding rounds) rather than just generic "we're interested" messages.

Take a look:

Example 1:

.webp)

Example 2:

.webp)

How can M&A advisors source higher-quality leads?

More leads doesn’t mean better leads. So the real advantage comes from targeting the right companies before outreach even begins.

And the solution lies in systematic pre-qualification.

- Set clear screening criteria upfront. Specify revenue thresholds, profitability minimums, customer concentration limits, and deal structure preferences before building target lists. This filtering prevents wasting months on companies that never fit your acquisition thesis.

- Go beyond firmographics. Track buying indicators like executive hires, technology stack changes, funding events, or competitive movements that suggest readiness for a transaction. Companies showing these signals convert 2–3× more often because timing aligns with their strategic needs.

Targeted cold email campaigns built around this data perform exceptionally well. Because they reach specifically qualified prospects with context-aware outreach.

The result is fewer total conversations, but much higher meeting-to-deal ratios. Advisors spend time with owners genuinely showing exit readiness rather than educating cold prospects about why they should consider selling.

How can you automate the M&A lead discovery process?

Automation in M&A lead gen helps teams scale their outreach while maintaining quality. That said, technology enhances rather than replaces human judgment in this space (and anyone telling you otherwise is trying to sell you software).

The reality is that automation works best for specific tasks in the discovery process such as:

- Pulling data from multiple sources

- Filtering based on predefined criteria

- Monitoring for trigger events (like exec changes or funding rounds)

- Managing outreach cadences

What it can’t do: The strategic thinking about which targets make sense, the relationship building that gets deals done, or the judgment calls about when to pursue an opportunity and when to walk away.

The goal is to free up advisors time for the high-value work, like the way Sutton Capital Partners scaled deal flow while staying focused on the right opportunities.

And cold outreach is one of the most useful applications. Done properly, it strikes a balance between scale and personalization.

It allows you to find decision-makers at target companies, personalize messages using live company data, track engagement and route responses directly into your CRM for fast follow-up.

What are the best strategies for efficiently managing an M&A deal pipeline?

Good pipeline management begins at the top of the funnel with consistent deal flow. That’s why advisors who depend on scattered inbound leads often face feast-or-famine cycles and rushed decisions.

So first, start by defining clear pipeline stages, each with specific criteria for moving forward. A typical structure includes:

- Initial Contact

- Qualification

- NDA Execution

- Preliminary Valuation

- LOI Negotiation

- Due Diligence

- Closing

Each stage needs defined entry and exit points. This prevents unqualified or stalled deals deals from lingering indefinitely without progress.

Second, consistent outreach solves the top-of-funnel problem by generating qualified conversations continuously. Targeted cold email campaigns can keep a steady flow of pre-qualified conversations moving through the pipeline.

This also gives advisors negotiating power (you're never desperate for a single deal to close) and allows selective focus on highest-potential targets.

And third, track velocity metrics religiously. Measure average days in each stage, conversion rates between stages, and reasons for pipeline exits.

For example if deals consistently stall during due diligence, you're likely targeting companies with incomplete financials. If qualified prospects don't convert to NDAs, your value proposition needs refinement.

If you’re wondering what a more predictable pipeline actually looks like in practice, the Winston Dunn case study shows how a structured outbound engine changed their deal flow.

Which M&A evaluation metrics should M&A advisors track?

Activity is not the same as progress. So start by splitting metrics into two categories:

- Activity metrics: calls made, emails sent, meetings held

- Outcome metrics: conversions, close rates, deal size, time-to-close

Pipeline conversion rates are essential. Track how deals move stage to stage:

- Initial Contact → Qualification: 15–25%

- Qualification → LOI: 30–40%

- LOI → Close: 60–75%

Dramatic drop-offs at specific stages diagnose exactly where your process breaks.

And you definitely need to track source effectiveness, as it identifies which channels produce closeable deals.

Track not just volume from each source (databases, referrals, cold outreach, events) but quality measured by close rate and average deal size. For example cold email campaigns often generate lower initial response rates than warm referrals but can produce higher volumes of qualified opportunities when properly targeted.

Frequently asked questions

Closing an M&A deal typically takes between 6 and 12 months, though the timeline often shifts depending on the deal's complexity regulatory requirements, and whether issues arise during due diligence.

Combining technology platforms with systematic outreach processes dramatically improves efficiency. Modern advisors use deal-sourcing databases to identify targets matching specific criteria, intent-based signals to find companies showing readiness indicators, and specialized lead generation services to reach decision-makers at scale with personalized messaging.

Main documents include confidentiality agreements, teasers, confidential information memoranda, letters of intent, due diligence materials across financial and legal areas, purchase agreements with representations and warranties, disclosure schedules, indemnification agreements, regulatory filings, and integration plans. Each document serves specific purposes at different process stages.

Qualifying targets means assessing how well they align on strategic, financial, operational, and cultural levels. Advisors use specific criteria, such as ensuring the target fits the acquisition strategy, meets financial benchmarks, has the operational strength to support integration, and aligns culturally to minimize risks during the process.

To make your deal-making process more efficient, consider creating standardized templates for your go-to documents and using a CRM system to track deals. You can also save time by automating data collection, thoroughly preparing before you start, and establishing clear communication to avoid asking for the same information twice.

Don’t miss these

Get your first lead this month

14 days to get started. 7 days to get your first lead on average.