M&A deal sourcing explained: Step-by-step deal origination guide

TL;DR

- The funnel is wide 📉 The average PE firm reviews ~80 opportunities to close one (≈1.25% conversion). Precision matters more than volume.

- Deal sourcing ≠ deal origination 🤝 Sourcing identifies and screens; origination includes long-term relationship and mandate development.

- Strong sourcing starts with clarity 🎯 Define sector, geography, revenue/EBITDA range, ownership profile, and valuation benchmarks before outreach.

- Build and tier your target universe 🗂️ Segment Tier 1–3 by strategic fit before contacting anyone.

- Timing beats volume 📬 Trigger-based outreach (leadership changes, funding, tenure milestones) generates 15–25% response rates vs 5–10% generic outreach.

- Qualification must be disciplined 📊 Use weighted scorecards and disqualify early (customer concentration, regulatory risk, misaligned management).

- Inbound creates opportunity; outbound creates predictability 🔄 Leading firms source 60–70% of deals from proactive channels.

- Accuracy beats scale 🔎 Smaller, signal-driven target lists outperform broad, poorly filtered universes.

M&A deal sourcing is the systematic process of identifying and qualifying acquisition targets before any formal transaction begins, and it's the phase where most firms are quietly bleeding time and opportunity. 📉

It sounds procedural, and in many ways it is.

Take the numbers: the average private equity firm evaluates 80 opportunities for every deal it closes, a conversion rate of just 1.25%. Behind that figure is real effort spent on companies that were never going to close, and real deals that were simply never found.

That said, sourcing done well is one of the most returnable investments a deal team can make. 💡

We've built and run outbound deal origination campaigns for investment banks and M&A advisory firms long enough to know where most programs quietly fall apart and this guide covers exactly how to fix that.

What is M&A deal sourcing?

M&A deal sourcing, sometimes called deal origination, is the systematic process through which dealmakers search for, identify, and match acquisition opportunities with defined investment criteria.

It is the first critical stage of the M&A lifecycle. It comes before due diligence and before deal execution.

The two terms are often used interchangeably. However, there is a practical distinction.

- Deal sourcing refers to identifying and screening targets. This includes mapping the market, making contact, and qualifying companies against clear criteria.

- Deal origination is broader. For investment bankers, it includes early relationship building and mandate development, often starting long before a specific target is identified.

In practical terms, M&A deal sourcing includes everything that happens before due diligence, before the LOI, and before a formal process begins. No transaction, whether proprietary or intermediated, reaches closing without passing through this stage first.

Because of that, sourcing is not a side activity. It is a structured discipline. (We often see teams treat it as opportunistic, which creates inconsistency over time.)

Many failed transactions trace back to weak early qualification rather than diligence surprises. The fit was imperfect from the beginning, but the screening process did not filter rigorously enough. 📊

How does the M&A deal sourcing process work?

The M&A deal sourcing process moves from defining an investment thesis through to a signed letter of intent, with each step building on the previous one. And because the funnel is wide, structure becomes essential.

Here is how the process usually works:.

Step 1: Define your acquisition criteria and investment thesis

Before any outreach begins, define exactly what you are looking for. The investment thesis typically specifies:

- Target sectors and geographies

- Company size by revenue and EBITDA

- Ownership stage, such as founder led, platform, or minority stake

In 2026, expected EBITDA multiples are approximately 6.8x for typical businesses and 9.8x for premium businesses, so criteria informed by real market pricing saves the team from chasing misfits.

Step 2: Build your target universe and segment by fit

Next, map the full universe of potential targets, then tier them by fit before initiating contact.

- Tier 1, highest strategic priority

- Tier 2, meets most criteria

- Tier 3, fits sector and size only

Common data sources include PitchBook,ZoomInfo, Capital IQ, SourceScrub, Crunchbase, and Cyndx for mid market and private company coverage.

Step 3: Choose your deal sourcing channels

Channel selection is a strategic decision, not a default. Deal sourcing channels typically fall into six categories:

- Investment banks and advisors

- Business brokers

- Direct proprietary outreach

- Referral networks

- Online deal platforms

- Industry events and conferences

The right mix depends on firm type, deal size, and target market.

Each channel carries distinct trade-offs in speed, cost, exclusivity, and deal quality, which we cover in the strategies section below.

Step 4: Execute initial outreach and engagement

Outreach in M&A is timing-driven, not volume-driven. 📬

A well-structured program times initial contact to observable trigger events that indicate a target may be more receptive: leadership changes, ownership tenure, funding events, or significant headcount shifts.

Research benchmarks make the case clearly: trigger-based outreach achieves response rates of 15 to 25%, compared to 5 to 10% for standard cold outreach. 📈

In practice, an individual business development professional typically maintains active outreach to 30 to 50 target companies at any one time, adding 10 to 20 new targets each month.

The outreach itself is rarely the bottleneck in deal sourcing. The bottleneck is almost always the lead list for cold outreach. Firms that reach the right 50 companies with a personalized, signal-driven sequence consistently outperform firms contacting 500 poorly qualified targets with generic messaging.

Step 5: Qualify and score potential targets

Not every company that responds to outreach belongs in your active pipeline.

A common scoring approach is the weighted scorecard, where each qualification dimension is assigned a weight reflecting its importance to the acquirer.

Targets scoring above 3.5 out of 5 advance. Those below that threshold don't, regardless of how interesting the initial conversation felt.

Three red flags warrant automatic disqualification: customer concentration above 40%, active regulatory investigations, and management unwilling to remain post-acquisition

Step 6: Manage relationships and your deal flow pipeline

Most M&A deals don't close after the first conversation. (Frankly, most don't close after the fifth, either.)

Long-term relationship management is what separates firms with consistent proprietary deal flow from those scrambling to compete in auction processes. 🤝

A structured M&A deal sourcing pipeline typically moves through defined stages:

- Target identified

- Outreach initiated

- In conversation

- Engaged

- Relationship developed

- Opportunity signal

- Process initiated

- Due diligence

- Closed

Different firms operate on different timelines. Corporate acquirers often maintain relationships over 3 to 5 years. Private equity firms typically work within 2 to 3-year cycles.

Either way, the discipline is the same: consistent, logged follow-ups over time.

Step 7: Progress qualified targets toward LOI

Once a target is qualified and strategically aligned, the progression typically looks like this:

- Introductory conversations

- Broader stakeholder engagement, finance, operating partners, BU leaders

- NDA execution

- Preliminary financial review

- Indication of Interest or Letter of Intent (LOI) 📝

A letter of intent (LOI) is the formal document that marks the transition from deal sourcing to deal negotiation. It signals seriousness on both sides.

Insider Tip: LOIs are rarely won in the LOI meeting. They are won in the months of disciplined, thoughtful engagement before it.

Targets that reach the LOI stage and beyond close at 40 to 60%. But make no mistake, the quality of that downstream process is almost entirely determined by how well the upstream sourcing stages were built.

📚 If you're curious about what happens after the LOI lands, we cover the full M&A process step by step.

What are the best M&A deal sourcing strategies?

The most effective M&A sourcing programs combine three lead generation strategies: inbound, outbound, and proprietary.

When people ask us what the best M&A deal sourcing strategy is, the honest answer is that it depends on what kind of firm you are and what kind of control you want over your pipeline.

Industry research shows that leading acquirers generate roughly 20 to 40% of deal flow from inbound sources, and 60 to 70% from outbound and proprietary channels.

Because inbound creates opportunity. But outbound and proprietary create predictability.

And because predictability matters in M&A, the mix matters too.

So let’s walk through each approach in practical terms.

Inbound M&A deal sourcing: How to make targets come to you

Inbound M&A deal sourcing refers to deal flow generated when targets or intermediaries initiate contact with your firm, rather than the reverse. 🔍

The main drivers are typically:

- Strong sector reputation

- Published thought leadership or proprietary research

- Conference visibility

- Referral networks through portfolio companies and advisors

When inbound works, it works well. You often see faster timelines, stronger founder alignment, and less competitive pressure. When someone calls you directly, it usually means there is intent behind it.

At the same time, inbound volume is naturally inconsistent. It rarely aligns perfectly with your acquisition criteria, and timing is entirely outside your control. (We have seen inbound pipelines swing dramatically based on market sentiment alone.)

If inbound is your only sourcing strategy, your pipeline depends on market conditions, not your effort. It needs to be paired with proactive M&A outbound lead gen work to build a pipeline that's actually predictable.

Outbound M&A deal sourcing: How to build your M&A prospecting engine

Outbound M&A deal sourcing refers to proactively identifying and reaching potential acquisition targets before they engage an intermediary or enter a formal sale process

A well-built outbound origination program runs on five components:

- A clearly defined, tiered target list, enriched with firmographic and behavioral data before any outreach begins

- Signal-based timing, where initial contact is tied to observable trigger events (leadership transitions, ownership tenure, funding rounds, headcount changes) that indicate a target may be more open to a conversation

- A sequenced outreach cadence of 3 to 5 touches across channels over 3 to 4 weeks

- Cold email personalization that addresses each target's situation directly, given that 71% of decision-makers ignore outreach that doesn't speak to their specific challenges.

- CRM-integrated follow-through, so every positive response is captured, tracked, and progressed without anything getting lost

We work with many investment banks and M&A advisory firms on exactly this model, researching contacts across a client's defined verticals each month and filtering by exit readiness signals (CEO tenure, company age, headcount changes, funding activity) before any outreach is sent.

For firms weighing whether to build this capability internally or partner externally, the honest reality is that standing up the signal-monitoring and list-building infrastructure alone takes most teams 3 to 6 months before quality outreach can begin. (And yes, that timeline usually catches people off guard.)

Proprietary M&A deal sourcing: Why getting to the deal first changes everything

Proprietary M&A deal sourcing is a form of outbound sourcing, with one critical distinction: you're reaching companies that have never been marketed through intermediaries and have no formal sale process underway.🥇

It is the most valuable sourcing strategy for a specific, measurable reason: proprietary deals have historically commanded a meaningful, double-digit discount on enterprise value compared to auctioned transactions.

The advantages are clear:

- Less competition

- Greater flexibility in structuring

- Stronger founder relationships

- More favorable economics

Top-performing PE firms dedicate 30 to 40% of deal team time to proactive, proprietary sourcing. Corporate development teams build proprietary flow by embedding business unit relationships into their sourcing process and maintaining long-term contact with target companies well before those companies are thinking about a transaction.

The firms consistently finding the best proprietary deals aren't necessarily better analysts. They're better at staying in front of the right people 12 to 18 months before those people are ready to transact.

How do you find and qualify acquisition targets efficiently?

Finding acquisition targets efficiently is less about volume and more about identifying the right signals. 🔎

The most reliable opportunities often show measurable indicators of transition readiness. These indicators generally fall into three categories:

- Ownership and exit-readiness signals

- Financial and operational trigger events

- Market and strategic trigger events

The right company at the wrong time rarely converts.

So let’s examine the signals more closely.

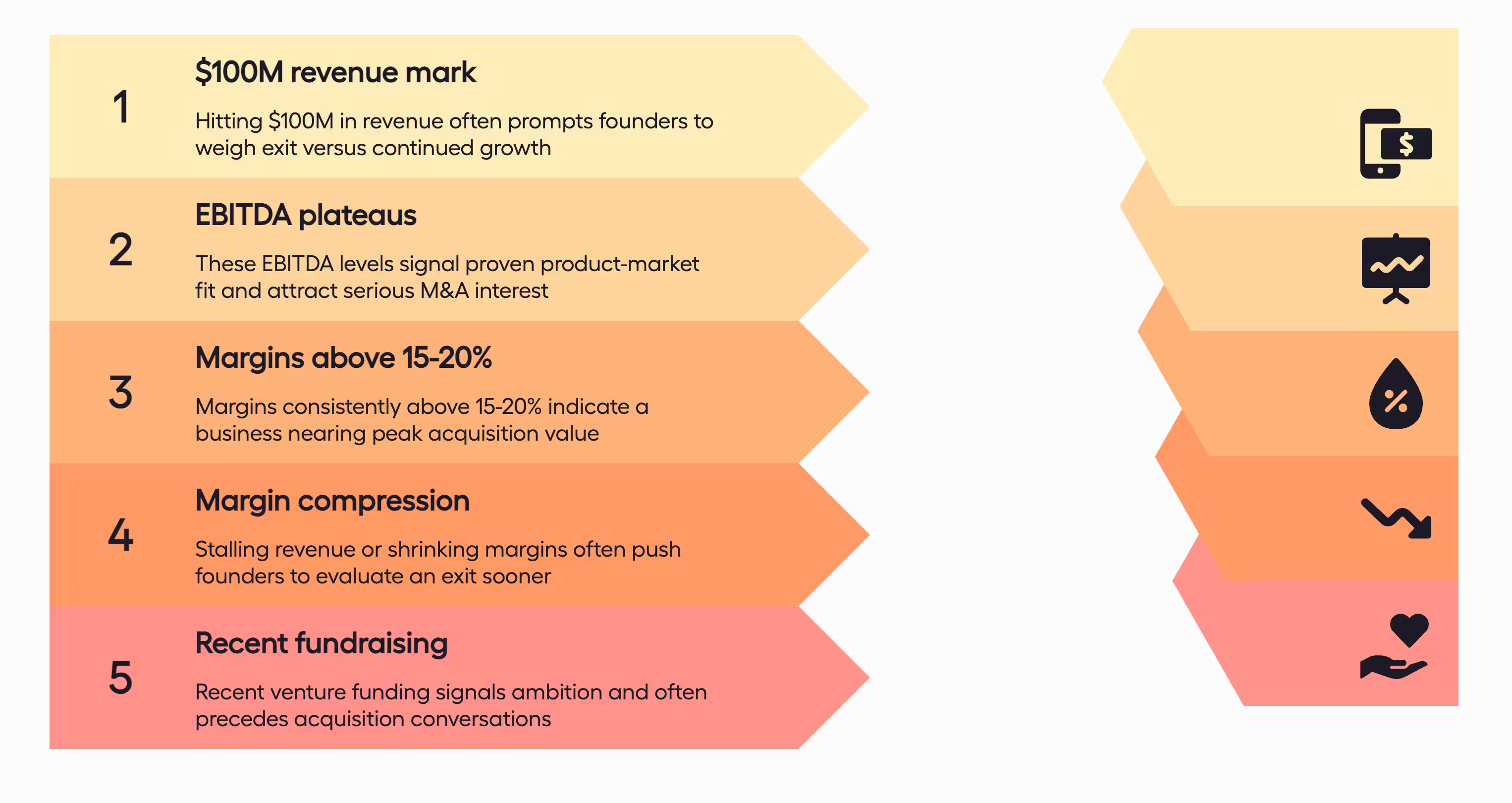

Ownership and exit-readiness signals

- 👤 Founder age is one of the most reliable ownership signals available. Founders over 60 are statistically more likely to consider exit options, often driven by retirement planning, wealth concentration in a single asset, or succession challenges with no clear internal heir.

- 📊 Ownership concentration matters too. Founders holding 80% or more of a business frequently become more exit-motivated as personal net worth grows increasingly tied to one company. Multi-founder businesses sometimes reach inflection points where co-founders' priorities diverge sharply, triggering a strategic review.

- ⏱️ Private equity hold period signals are worth monitoring in your target list. The typical hold period sits at 4 to 6 years.

- 🏢 ESOP dynamics create a less obvious trigger. When an ESOP trust accumulates significant company ownership, governance and liquidity pressures sometimes push owners toward a transaction with an external buyer.

Financial and operational trigger events

Financial inflection points often create natural exit conversations.

Here are the most common triggers:

When owners reach personal financial goals, they frequently reconsider risk exposure. On the other hand, declining margins can accelerate exit discussions.

Management transitions are equally powerful signals. A founder stepping back and hiring an external CEO often indicates preparation for institutional growth. Unexpected executive turnover can signal deeper strategic tension.

Market and strategic trigger events

External pressure frequently accelerates acquisition decisions.

Key triggers in this category include:

- Regulatory shifts increasing compliance burden

- Technology disruption affecting competitiveness

- Competitor acquisitions within the same sector

- Capital requirements exceeding current ownership appetite

How do you improve the accuracy of your M&A target list?

A large target list feels productive.But in practice, it often means a lot of wasted outreach on companies that should have been filtered out before the first email was drafted. 🔍

Accuracy comes from layering data before you act on it: firmographic enrichment (revenue, headcount, funding history), technographic mapping (what tools they run), and behavioral signals (recent hiring trends, leadership changes).

From there, sequential filtering against your thesis cuts the list down to companies that actually fit.

Lookalike modeling goes one step further, using characteristics from past successful deals to surface structurally similar companies you might have otherwise missed. And with nearly 50% of dealmakers using AI screening tools in 2025, that process has gotten significantly faster.

A long target list is only valuable if it's accurate. Every hour spent qualifying a company that should never have made the list is an hour not spent on one that genuinely fits. The goal of enrichment and filtering is to make your active outreach list smaller, not bigger.

What are the main M&A deal sourcing channels?

As we mentioned earlier, the six primary M&A deal sourcing channels are investment banks and advisors, business brokers, direct proprietary outreach, referral networks and online deal platforms.

But now let’s look at how they compare side by side, because where you invest time and budget directly shapes pipeline quality and exclusivity.

What tools are used for M&A deal sourcing?

M&A deal sourcing typically relies on two distinct tool categories:

First, there are CRM and relationship intelligence platforms, designed to manage active pipeline and long-term contacts.

Second, there are private market intelligence platforms, used to identify and research target companies.

And these categories serve different functions. One manages relationships. The other finds opportunities.

So with that in mind, let’s look at each group more closely.

CRM and relationship intelligence platforms

CRM and relationship platforms help track conversations, follow-ups, and multi-year relationship cycles. In M&A, that visibility is critical because timelines are rarely short. (Most deals develop over months or years.)

Common platforms include:

- DealCloud

- Affinity

- Hubspot

- Salesforce

Even the best CRM fails without discipline. Logging interactions, setting follow-ups, and running weekly reviews matter more than feature depth.

Which software helps you identify the right companies to acquire?

Private market intelligence platforms on the other hand focus on discovery and research rather than pipeline management.

They help answer a simple but difficult question: Which companies actually fit our criteria?

The most widely used tools include:

- SourceScrub

- ZoomInfo

- PitchBook

- Capital IQ (FactSet)

- Axial

- Crunchbase

- Cyndx

How can you automate and speed up your M&A prospecting process?

Automation has meaningfully changed M&A prospecting workflows in recent years. Nearly 50% of dealmakers reported using AI tools for sourcing, screening, and diligence in 2025.

And there are four areas that drive most of the acceleration:

- Automated data enrichment: Extracts and continuously updates company profiles from websites, filings, social media, and news without manual research.

- AI-powered screening:Rapidly evaluates large company sets against acquisition criteria and surfaces patterns from past successful deals.

- Workflow automation: Manages email sequencing, scheduling, and call transcription to reduce manual workload.

- LLMs: Summarize company information, compare competitors, and draft investment memoranda, compressing research cycles significantly .

That said, automation requires oversight.

Automation without quality control perpetuates bad data and can generate high-volume outreach that damages brand reputation. Automated systems are only as reliable as the data and models behind them.

Sourcing is where M&A deals are won or lost

Most M&A teams already know what good sourcing looks like in theory. Tiered target lists, exit-readiness signals, a structured outreach cadence, a CRM that actually gets used.

The framework isn't the hard part.

The hard part is Tuesday morning when two live deals are demanding attention, three intermediaries are waiting on callbacks, and the "proactive sourcing" work that was supposed to happen this week quietly gets pushed to next week. And then the week after that.

We've seen this pattern enough times that it stopped surprising us. Sourcing requires dedicated, consistent effort that competes directly with the work that feels more urgent on any given day.

And if that sounds familiar and you'd like a hand getting a structured outbound program running without adding headcount, we'd genuinely love to talk through what that looks like for your firm.

Frequently asked questions

M&A deal sourcing refers to the identification and initial screening of acquisition targets. Deal origination is broader; it encompasses sourcing and the early relationship-building that follows, and for investment bankers, the mandate-winning process.

The best deal sourcing channels depend on firm type and deal size. Proprietary outreach and referral networks deliver the highest quality and exclusivity; investment bank relationships produce the most volume. Leading firms allocate 60 to 70% of sourcing effort to outbound and proprietary channels.

PE firms use a multi-channel approach: proprietary outreach, investment bank relationships, business broker networks, and operating partner referrals. Top-quartile firms allocate 30 to 40% of deal team time to proactive sourcing, with 60 to 70% of deal flow coming from proprietary channels.

Speed in M&A prospecting comes from three key sources: tiered target lists, signal-based outreach timing that focuses effort on exit-ready companies, and automation of data enrichment and email sequencing. None require sacrificing qualification standards; they shift effort from volume to precision.

Building proprietary M&A deal flow from scratch requires a defined target sector, consistent outreach to non-marketed companies, dedicated relationship management resources, and formalized advisory relationships. This typically requires 2 to 3 years of sustained effort to produce consistent proprietary flow.

Don’t miss these

Get your first lead this month

14 days to get started. 7 days to get your first lead on average.